Payday loan rates vary from state to state. In this guide from Pheabs, we’ll run through the information you need to find out the typical rates you should expect from a payday loan.

According to the Consumer Financial Protection Bureau, a standard two-week payday loan will carry a charge of $10 to $30 on every $100 borrowed depending on state regulations. Put in context, a low-end rate of $15 per $100 would come to an annual interest rate of 400%. By comparison, the average APR for another form of borrowing, credit cards, is 15.09%, according to the Federal Reserve.

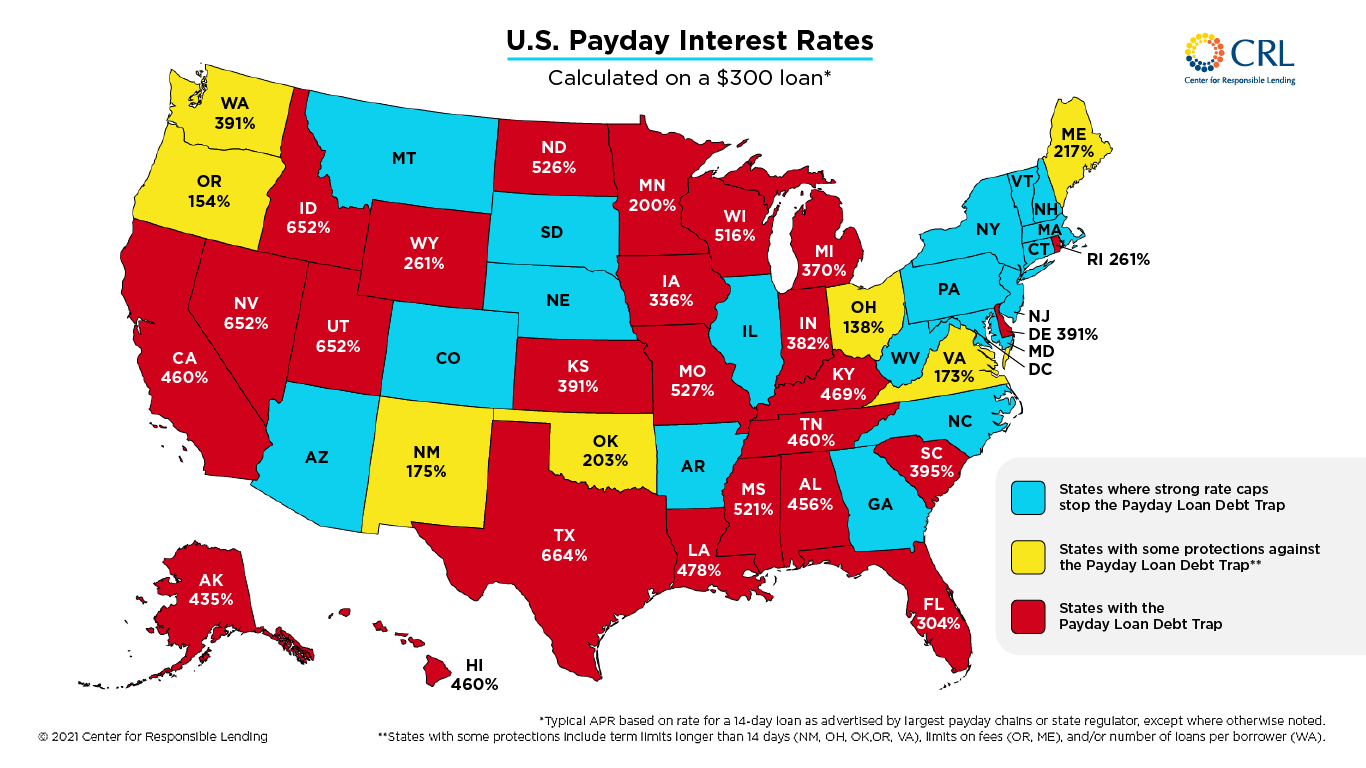

According to the Center for Responsible Lending, the average APR in Nevada, for example, is 652%. In contrast, states with more protections see far lower average APRs. Virginia, for example, has a 254% average interest rate.

Why Do The Typical Rates For A Payday Loan Vary By State?

An annual percentage rate (APR) is the value given to denote the yearly interest rate charged to borrowers. APR represents the actual annual cost over the term of a loan. For short-term payday loans, the APR is partially determined by state-level restrictions. Payday loan APRs regularly reach three figures, and in some cases, four figures! Four states don’t have any interest-rate caps at all. For example, in Missouri, an APR as high as 1,950% for a loan of $100 for 14-days would be permitted.

Why Are Typical Payday Loan Rates Higher Than Other Loans?

The rates associated with payday loans are higher than the rates of some other loans because APR factors in time. Those applying for a payday loan are typically in a financial emergency that cannot wait until payday. As a result, they may be looking to borrow for a short amount of time, around 2-4 weeks, until their next check comes.

Lenders also claim the high rates are necessary because of the high risk involved with this kind of lending. Payday loans are targeted toward consumers in need of money fast. They are generally easy to receive compared to other borrowing forms. A customer would only need a valid ID, proof of income, and a checking account to be approved in most cases.

Credit checks are often discarded to approve applicants quickly. As a result, lenders justify the extremely high rates because of the increased risk that comes with the loan. Lenders don’t have the security that consumers will pay the loan back, and, unlike a mortgage or car loan, there’s typically no collateral either.

How Are Payday Loan Rates Calculated?

Payday loan rates are typically calculated based on the amount borrowed and the length of the loan term. For example, a lender may charge $15 in fees for every $100 borrowed, which would result in a 15% rate for a two-week loan term.

How Can I Compare Payday Loan Rates?

To compare payday loan rates, you can look at the fees charged by different lenders and calculate the APR based on the length of the loan term. You can also use online comparison tools that allow you to enter the amount you want to borrow and the length of the loan term to see a comparison of rates from different lenders.

Can Payday Loan Rates Be Negotiated?

Payday loan rates are typically set by the lender and may not be negotiable. However, you may be able to negotiate the terms of the loan, such as the repayment schedule or the fees charged. Make sure to read the loan agreement carefully and ask any questions you may have before agreeing to the loan.

Are There Any Regulations on Payday Loan Rates?

Payday loan rates are regulated at the state level, and the regulations vary widely by state. Some states have banned payday lending altogether, while others have placed caps on the amount lenders can charge in fees or interest. The Consumer Financial Protection Bureau (CFPB) has proposed federal regulations on payday lending, although these regulations have not yet been fully implemented.

What Are The Typical Rates For A Payday Loan In Each State?

The following table details the APR for a $300 loan in each state. Source: Center For Responsible Lending.

{kind=link}

State | Payday loan APR for a $300 Loan |

| Alabama (AL) | 456.25% |

| Alaska (AK) | 520% |

| Arizona (AZ) | 204% |

| Arkansas (AR) | 280% |

| California (CA) | 460% |

| Colorado (CO) | 36% |

| Connecticut (CT) | N/A (payday loans are prohibited) |

| Delaware (DE) | N/A (payday loans are regulated, but there is no cap on interest rates) |

| Florida (FL) | 304% |

| Georgia (GA) | N/A (payday loans are prohibited) |

| Hawaii (HI) | N/A (payday loans are prohibited) |

| Idaho (ID) | 52.73% |

| Illinois (IL) | 404% |

| Indiana (IN) | 391% |

| Iowa (IA) | 433% |

| Kansas (KS) | 390% |

| Kentucky (KY) | 459% |

| Louisiana (LA) | 391% |

| Maine (ME) | N/A (payday loans are prohibited) |

| Maryland (MD) | N/A (payday loans are prohibited) |

| Massachusetts (MA) | N/A (payday loans are prohibited) |

| Michigan (MI) | 369% |

| Minnesota (MN) | 390% |

| Mississippi (MS) | 521.43% |

| Missouri (MO) | 1950% |

| Montana (MT) | 36% |

| Nebraska (NE) | 460% |

| Nevada (NV) | 652% |

| New Hampshire (NH) | 36% |

| New Jersey (NJ) | 30% |

| New Mexico (NM) | 175% |

| New York (NY) | N/A (payday loans are prohibited) |

| North Carolina (NC) | N/A (payday loans are prohibited) |

| North Dakota (ND) | 487.50% |

| Ohio (OH) | 28% |

| Oklahoma (OK) | 390% |

| Oregon (OR) | 154% |

| Pennsylvania (PA) | N/A (payday loans are prohibited) |

| Rhode Island (RI) | 260% |

| South Carolina (SC) | 390% |

| South Dakota (SD) | N/A (payday loans are prohibited) |

| Tennessee (TN) | 460% |

| Texas (TX) | N/A (payday loans are regulated, but there is no cap on interest rates) |

| Utah (UT) | N/A (payday loans are regulated, but there is no cap on interest rates) |

| Vermont (VT) | N/A (payday loans are prohibited) |

| Virginia (VA) | 687.76% |

| Washington (WA) | 391% |

| West Virginia (WV) | 460% |

| Wisconsin (WI) | 574% |

| Wyoming (WY) | 780% |

How Can I Get the Best Payday Loan Rates?

To get the best payday loan rates, you should shop around and compare rates from different lenders. Pheabs can do this for you by comparing the market and finding you the best lender to meet your unique needs. Fill in our short form and get a free quote.

You should also make sure you understand all the fees and repayment terms before agreeing to a loan. You may also be able to get a lower rate if you have a good credit score or if you are a repeat customer with a lender.

Can I Refinance a Payday Loan to Get a Lower Rate?

Some lenders may offer payday loan refinancing, which allows you to extend the loan term and pay lower fees or interest. However, refinancing a payday loan can be expensive and may lead to more debt in the long run. If you are struggling to repay a payday loan, it’s a good idea to contact the lender and see if they can offer you a payment plan or other options to help you avoid defaulting on the loan.

Last Updated on June 13, 2024 by Daniel Tannenbaum, Founder of Pheabs